With this backdrop... Minnesota's mortgage lenders now face the uncertainties created by the implementation of the definition of "Qualified Residential Mortgage" (Section 941) of the Dodd-Frank Reform Act. This section of the Act will require all financial institutions that securitize mortgage loans to retain at least five percent of the credit risk, and proposes strict definitions for Qualified Residential Mortgages that can be securitized.

Two of the Minnesota Homeownership Center's partners, Minnesota Housing Partnership and Wells Fargo will be hosting two events offering affordable housing advocates, lending and Real Estate professionals the opportunity to learn more about the Dodd-Frank Financial Reform Act and how the definition of Qualified Residential Mortgages may impact affordable homeownership in Minnesota and the country.

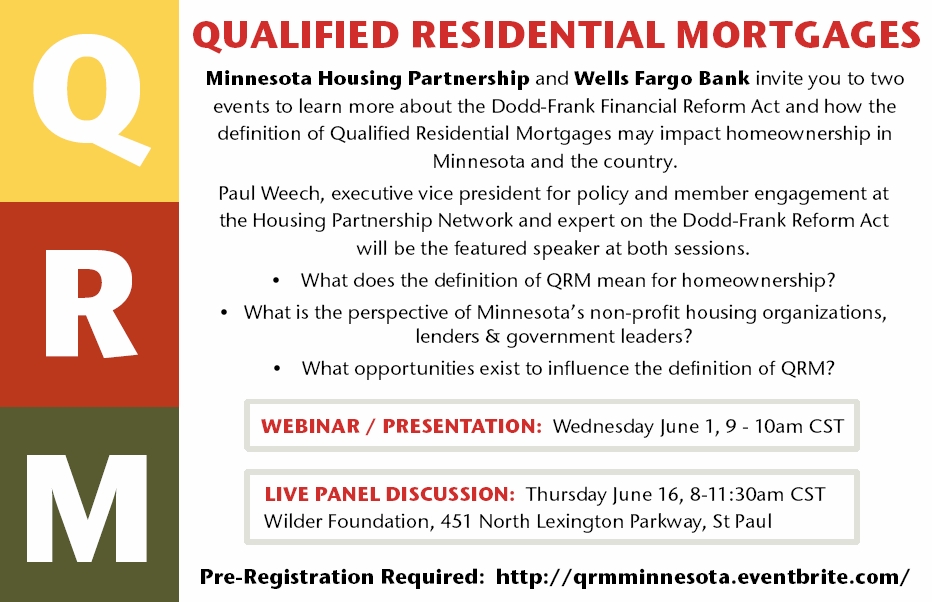

Paul Weech, executive vice president for policy and member engagement at the Housing Partnership Network and expert on the Dodd-Frank Reform Act will be the featured speaker at both sessions.

Participants will learn about:

- What does the definition of QRM mean for homeownership?

- What is the perspective of Minnesota’s non-profit housing organizations, lenders & government leaders of QRM?

- What opportunities exist to influence the final definition of QRM?

SESSION 1: Webinar

Date & Time: Wednesday, June 1st, 9-10am CST

SESSION 2: Live Panel Discussion

Date & Time: Thursday, June 16th, 8 - 11:30am CST

Location: Wilder Foundation, St. Paul, MN

To register (pre-registration required) or to learn more about the topics covered, visit the registration page here: http://qrmminnesota.eventbrite.com/