On Thursday December 1st, Fannie Mae and Freddie Mac both announced eviction moratoriums that will take place over the holidays. From December 19 through January 2, families living in properties where a Fannie Mae or Freddie Mac loan has been foreclosed upon will not be evicted.

NOTE: The legal and administrative processes for the evictions may continue during this time, but families will be able to stay in their homes. In addition, the GSE's will continue with the foreclosure process on delinquent borrowers during this time period as well.

Large mortgage servicers often follow suit – we will updated this blog if we learn of additional banks or servicers initiating moratoriums.

There are some nuances to the Fannie and Freddie moratoriums; additional details are available in the press releases here and here.

There is no "cold weather" rule regarding foreclosure or evictions after foreclosure in Minnesota. If you are struggling with mortgage payments or have questions about the process, contact a FREE non-profit Homeownership Adviser that specializes in foreclosure prevention TODAY. Waiting limits your options!

Friday, December 2, 2011

Monday, November 14, 2011

Southwest Minnesota Housing Partnership Awarded USDA Housing Preservation Grant

|

| Used under Creative Commons License. Photo by ario_ |

The Southwest Minnesota Housing Partnership (SWMHP) has been selected to receive a $69,000 Housing Preservation Grant through USDA Rural Development. The grant will be used to assist 11 very-low and low-income households in the cities of St. James, Sleepy Eye, Winthrop, Gibbon and New Auburn make essential improvements and repairs to their homes.

SWMHP is a member of the Center's Homeownership Advisors Network and offers Home Stretch workshops and counseling, refinance counseling and foreclosure prevention services in dozens of counties in Southwest Minnesota.

The Housing Preservation Grant program provides funding to intermediaries such as town or county governments, public agencies, federally recognized Indian Tribes, and non-profit and faith-based and community organizations. These organizations then distribute the grants to homeowners and owners of multi-family rental properties or cooperative dwellings who rent to low- and very-low-income residents.

Grants may be used to make general repairs, such as installing or improving plumbing or providing or enhancing access to people with disabilities. Funds may also be used to weatherize and make homes more energy efficient.

To learn more about the Southwest MN Housing Partnership, visit their website at http://www.swmhp.org/.

Improvement and rehab programs available through the Southwest MN Housing Partnership are included in the Center's "Repair and Rehab Matrix" that we've created as a resource listing improvement, rehab and repair programs in local communities throughout the state. Programs included in the Matrix include:

- emergency repair,

- energy efficiency,

- lead hazard abatement, and

- general repair.

Some funds are grants and others are loans, usually with below market interest rates. Looking for help with repair or rehab on your home? Visit the matrix page of the Center's website here: http://www.hocmn.org/en/rehab.cfm

Wednesday, November 9, 2011

Racial Disparities in Assets and Homeownership

|

| © Mullica |

The Minnesota Budget Project has reported that according to the American Community Survey (ACS) released by the U.S. Census Bureau last month, not only is poverty increasing in Minnesota, but disparities in poverty levels and household incomes between communities of color and whites are worsening. While the 2010 ACS reports that just under 12% of Minnesotans were living in poverty, the percentages according to race reveal a marked difference in poverty levels for communities of color--the highest being for American Indians which grew from approximately 31% in 2007 to just under 40% in 2010. Likewise, the median household incomes for Latino, black, and American Indian communities remain substantially lower than the statewide median household income for whites. Minnesota has historically suffered from racial disparities and, unfortunately, the latest reports do not hint towards the end of that plight.

On a national level, Minnesota’s averages rank on the better end for overall poverty levels and median incomes. Again, though, when looking more specifically at communities of color, Minnesota’s ranking drops significantly. In fact, the poverty rate in Minnesota for Asians is just over 5 percentage points greater than the national average while for both blacks and American Indians the poverty rate sits as high as 10 percentage points greater than the national average.

These racial disparities are all too often found in homeownership rates as well.

In 2010, John Patterson and Michael Grover reported that the homeownership rate for emerging markets communities was more than 30% below the homeownership rate for whites - the 5th largest gap in homeownership rates in the country. Furthermore, the recent housing crisis has hit the emerging market community especially hard with mortgage delinquencies and foreclosures. While the homeownership gap appears to be narrowing, there is still a need to reach this population with homeownership education and opportunities.

In an effort to confront these issues in Minnesota, the Center leads the Emerging Markets Homeownership Initiative (EMHI) which works to develop systemic changes within the homeownership industry to increase homeownership opportunities for communities of color. Developing culturally-specific resources and services for emerging market consumers is a key component of this initiative. To learn more about EMHI events and resources offered by the Center, visit the EMHI page of our website, here.

FREE Continuing Education (CEUs) for real estate professionals!

Learn more about the issues that Emerging Markets face and the efforts to achieve parity in homeownership rates in Minnesota at the FIFTH ANNUAL EMERGING MARKETS HOMEOWNERSHIP INITIATIVE SUMMIT. Learn more about the Summit, and register, here. The event has sold out in the past and we anticipate that it will sell out this year as well. Register today.

Learn more about the issues that Emerging Markets face and the efforts to achieve parity in homeownership rates in Minnesota at the FIFTH ANNUAL EMERGING MARKETS HOMEOWNERSHIP INITIATIVE SUMMIT. Learn more about the Summit, and register, here. The event has sold out in the past and we anticipate that it will sell out this year as well. Register today.

Thursday, November 3, 2011

Stripping Off Second Mortgages in Bankruptcy

The Minnesota Homeownership Center and the Housing Preservation Project have developed a new fact sheet that outlines the recent changes to Chapter 13 bankruptcy allowing 2nd mortgages to be stripped off if they are wholly underwater.

Prior to a ruling in "Fisette v. Keller" (actually court documents, here, if you're interested) this summer, limitations in the Bankruptcy Code prevented a mortgage on a principal residence from being modified in a Chapter 13 bankruptcy. Now, various courts have held that when the amount of the first mortgage is more than the value of the property, the second and third mortgages - and any other junior mortgages - are no longer secured and the limitation on modification no longer applies. These underwater second and third mortgages can be treated as unsecured claims, similar to credit card debt, and stripped off (removed or cancelled) by a Chapter 13 plan.

The fact sheet defines when second mortgages may be "stripped off" - and when they can't.

The Center is continually developing and updating our fact sheets around foreclosure prevention and homebuyer services. Visit our website often for the most recent versions of these documents... they're free to download and distribute!

Prior to a ruling in "Fisette v. Keller" (actually court documents, here, if you're interested) this summer, limitations in the Bankruptcy Code prevented a mortgage on a principal residence from being modified in a Chapter 13 bankruptcy. Now, various courts have held that when the amount of the first mortgage is more than the value of the property, the second and third mortgages - and any other junior mortgages - are no longer secured and the limitation on modification no longer applies. These underwater second and third mortgages can be treated as unsecured claims, similar to credit card debt, and stripped off (removed or cancelled) by a Chapter 13 plan.

The fact sheet defines when second mortgages may be "stripped off" - and when they can't.

The Center is continually developing and updating our fact sheets around foreclosure prevention and homebuyer services. Visit our website often for the most recent versions of these documents... they're free to download and distribute!

Wednesday, November 2, 2011

Independent Foreclosure Reviews

Banks have begun complying with enforcement action. Homeowners may be able to receive compensation on foreclosures conducted in 2009 and 2010

Under enforcement actions taken by the Office of the Comptroller of the Currency (OCC), the Federal Reserve, and Office of Thrift Supervision, more than a dozen large mortgage servicers are required to correct a number of problems with their servicing, loss mitigation and foreclosure processes. These servicers are also required to engage independent firms to conduct reviews of foreclosure activities that took place during 2009 and 2010.

Borrowers are eligible to submit a Request for Review to the independent consultants IF:

BE CAREFUL!!

National media outreach will begin soon, and millions of homeowners will be notified by mail about the review process and will receive instructions for submitting a five-page Request for Review Form. As with any major announcement of this kind, we anticipate a number of copycat services and scams to pop up.

The independent reviews are free of charge and homeowners should never have to pay for foreclosure intervention services.

If anyone asks you to pay for their help with a review... or sends you to a website other than the national website that has been set up by the OCC, be careful... it might be a scam!

The national website is: http://www.independentforeclosurereview.com/

Additional Information:

Requests for Review must be received by April 30, 2012. The independent consultants will confirm receipt of the form within one week, though the full reviews are expected to take several months to complete. The consultants will evaluate whether the homeowner suffered financial injury through servicer errors, misrepresentations or deficiencies in their foreclosure practices. In cases where findings indicate a homeowner suffered financial injury as a result of servicer practices, compensation or other remedies will be provided. The exact form of remediation is uncertain.

A copy of the OCC news release is here.

Participating Lenders and Servicers (As of 11/2/2011)

America’s Servicing Co.

Aurora Loan Services

Bank of America

Beneficial

Chase

Citibank

CitiFinancial

CitiMortgage

Countrywide

EMC

EverBank/EverHome Mortgage Company

GMAC Mortgage

HFC

HSBC

IndyMac Mortgage Services

MetLife Bank

National City Mortgage

PNC Mortgage

Sovereign Bank

SunTrust Mortgage

U.S. Bank

Wachovia Mortgage

Washington Mutual (WaMu)

Wells Fargo Bank, N.A.

Under enforcement actions taken by the Office of the Comptroller of the Currency (OCC), the Federal Reserve, and Office of Thrift Supervision, more than a dozen large mortgage servicers are required to correct a number of problems with their servicing, loss mitigation and foreclosure processes. These servicers are also required to engage independent firms to conduct reviews of foreclosure activities that took place during 2009 and 2010.

Borrowers are eligible to submit a Request for Review to the independent consultants IF:

- their loan was serviced by one of the 14 servicers or their affiliates (see list below),

- the property is, or was, their primary residence, and

- their loan was “active in the foreclosure process” between 1/1/2009 and 12/31/2010.

Active in the process can mean:

- Sheriff’s sale occurred on the property

- Loan was referred to foreclosure but the sale did not take place due to a payment plan, modification, or non-retention option; and

- Loans were referred to foreclosure but are still in delinquency.

BE CAREFUL!!

National media outreach will begin soon, and millions of homeowners will be notified by mail about the review process and will receive instructions for submitting a five-page Request for Review Form. As with any major announcement of this kind, we anticipate a number of copycat services and scams to pop up.

The independent reviews are free of charge and homeowners should never have to pay for foreclosure intervention services.

If anyone asks you to pay for their help with a review... or sends you to a website other than the national website that has been set up by the OCC, be careful... it might be a scam!

The national website is: http://www.independentforeclosurereview.com/

Additional Information:

Requests for Review must be received by April 30, 2012. The independent consultants will confirm receipt of the form within one week, though the full reviews are expected to take several months to complete. The consultants will evaluate whether the homeowner suffered financial injury through servicer errors, misrepresentations or deficiencies in their foreclosure practices. In cases where findings indicate a homeowner suffered financial injury as a result of servicer practices, compensation or other remedies will be provided. The exact form of remediation is uncertain.

A copy of the OCC news release is here.

Participating Lenders and Servicers (As of 11/2/2011)

America’s Servicing Co.

Aurora Loan Services

Bank of America

Beneficial

Chase

Citibank

CitiFinancial

CitiMortgage

Countrywide

EMC

EverBank/EverHome Mortgage Company

GMAC Mortgage

HFC

HSBC

IndyMac Mortgage Services

MetLife Bank

National City Mortgage

PNC Mortgage

Sovereign Bank

SunTrust Mortgage

U.S. Bank

Wachovia Mortgage

Washington Mutual (WaMu)

Wells Fargo Bank, N.A.

As always... if you have any questions about this Independent Foreclosure Review or are looking for ways to prevent the foreclosure of your home, contact a FREE, Non-Profit foreclosure prevention counselor that is a member of the Homeownership Advisors Network! To find your local counselor, click here.

Monday, October 31, 2011

Fifth Annual EMHI Summit - Registration Open

Exciting Changes This Year!

This year’s annual Summit reflects the dynamic field by hosting a variety of rapid learning stations for participants to gain valuable knowledge through several 15-minute sessions. We hope our new format for the event will make you better prepared to seize opportunities and confront challenges surrounding homeownership for emerging markets.

This year’s event will be fast-paced and informative for professionals looking for insight into the current status of emerging market homeownership in the State of Minnesota.

The morning session will begin with a keynote address from Dorothy Bridges, recently-appointed Vice President of Community Development and Outreach at the Federal Reserve Bank of Minneapolis.

Following the address, Summit participants will have the opportunity to rotate among various rapid learning stations hosted by leaders in the emerging market homeownership arena to get a snapshot of current issues and trends facing the industry. Stations will also be a time for participants to ask questions and gain best practice tips from leaders and colleagues in the profession. Some learning station topics include:

- Financial Literacy,

- Housing and Transportation Corridor Issues,

- Minnesota Housing and Bond Programs,

- Federal Housing Administration,

- Demographics,

- And MANY more!

3.5 hours of Real Estate CEU credits have been applied for.

-----------------------------------------

Want to dig deeper into homeownership and emerging markets issues?

This year we are also pleased to announce an optional afternoon session! We have invited Susan Didier, President of Thompson Associates, to teach her newly-developed course for the Minnesota Association of REALTORS® entitled, Emerging Markets: The New-American Homebuyer. Her course covers everything from cultural diversity issues such as language barriers and cultural values to explaining real estate in the real world, which highlights topics such as buyer readiness and special first-time homebuyer products. This afternoon course counts towards 3.75 hours of CEU credits.

-----------------------------------------

Last year's Summit sold out so register early!

Thursday, October 27, 2011

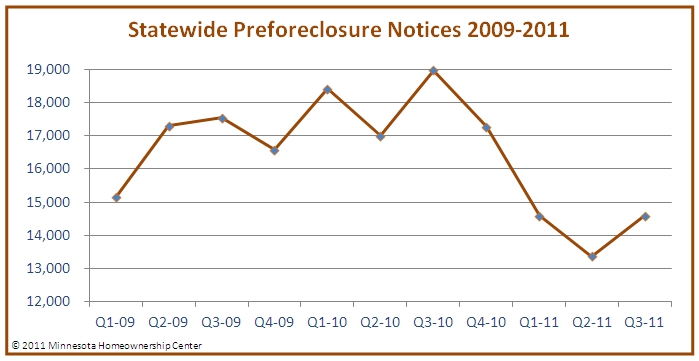

Preforeclosure Notices, 3rd Quarter - A Mixed Bag

Preforeclosure Notices Send Mixed Signals for Housing in Minnesota

On Thursday, October 27th, the Minnesota Homeownership Center released its third quarter data on the aggregate number of Preforeclosure Notices received by foreclosure counselors in the Homeownership Advisors Network. The numbers continue to show that Minnesota is slowly emerging from the foreclosure crisis, while also signaling reasons for the state to continue to make fighting foreclosures a priority: the number of preforeclosure notices received in the third quarter of 2011 signals the first uptick in quarterly notices in a year.

In the third quarter of 2011, members of the Homeownership Advisors Network received 14,586 preforeclosure notices, 23% fewer than during the same time period in 2010, but an increase of 9% from the second quarter of 2011, when 13,372 notices were received.

|

| Click To Enlarge |

Most troubling is that 85% of the increase in notices from Q2 to Q3 came from the Twin Cities metro… with 43% of the increase coming from Hennepin County alone, which saw an increase of more than 500 preforeclosure notices. Is this a statistical outlier or the beginning of a troubling trend? The Minnesota Homeownership Center will continue to track these notices and will report on the Q4 and year-end numbers in early 2012.

The total number of preforeclosure notices received in the state of Minnesota in 2011 now exceeds 42,000:

|

| Click To Enlarge |

Here's the breakdown for the number of preforeclosure notices received by members of the Homeownership Advisors Network in the 7-county metro area:

|

| Click To Enlarge |

As background for new readers, Minnesota state law (MN Statute 580.021) requires that the foreclosing party provide information regarding foreclosure prevention counseling services to the mortgager (homeowner) and provide the homeowner’s name, address, and most recent known telephone number to an approved foreclosure prevention counseling agency before filing the notice of pendency.

Once the Minnesota Homeownership Center's network of foreclosure counselors receives notification from the lender/servicer/homeowners association, they then contact the homeowner, and track the number of notifications received during the month in their monthly reporting to the Center.

If you or someone you know is struggling with their mortgage payment, new programs, resources and assistance are becoming available all the time. Don’t give up… contact a foreclosure counselor that is a member of the Homeownership Advisors Network today to see if there’s help available for you to avoid foreclosure. Even if you’re not yet behind, now is the time to call. To find your local foreclosure counselor, click here.

Monday, October 24, 2011

HARP Changes - What We Know, What We Don't

It is likely that President Obama will be announcing some major changes to the Home Affordable Refinance Program (HARP) on Monday, October 24th, 2011. The Federal Housing Finance Agency, the agency that regulates Fannie Mae and Freddie Mac as well as the 12 Federal Home Loan Banks throughout the country, has issued a press release outlining some of the important changes to the HARP program.

What We Know:

What We Know:

- The goal is to prevent additional foreclosures by allowing additional underwater homeowners to refinance their mortgages at today's low interest rates and/or shortening the term of their mortgage.

- Most importantly, the current 125% Loan to Value limit (LTV Ceiling) will be removed, but there is still a MINIMUM LTV of 80%. Borrowers that are underwater by any amount greater than 80% may be able to participate in HARP.

- Borrowers fees to participate in HARP will be reduced.

- To participate, borrowers must be current, have not been late on a payment in the last 12 months, and have a verifiable source of income. Actual affordability ratio (how much income needed) has not been released.

- The new guidelines should waive the need for a full appraisal if a reliable Automated Valuation Model (AVM) is available on the property.

- Participation in HARP is a one-time opportunity. If a homeowner has refinanced under the original HARP guidelines, they will NOT be able to refinance a second time under these new changes.

- Only mortgages that are owned by the Government Sponsored Enterprises (GSE's), -- Fannie Mae and Freddie Mac -- will be participating in the new program. The mortgage must have been sold to Fannie Mae or Freddie Mac on or before May 31, 2009. To determine if your loan is owned by Fannie or Freddie, you can use the following links:

What We Don't Know

This blog post was written on Monday 10/24/2011... and many of the details may change over time. Please call a non-profit housing counselor for additional details about these HARP changes... or any other question you may have about your mortgage.

- When will homeowners actually be able to refinance their Freddie Mac- or Fannie Mae-backed mortgage? Guidelines on the new program will be sent to lenders and servicers by November 15th. After that, the lenders/servicers will have to convert those guidelines into actual policies and procedures. This means that it may be mid-December or even early 2012 before a homeowner can actually participate. In addition, the concept of the program is complicated by the fact that certain servicers DO NOT ORIGINATE loans and may not have the capacity to originate the new HARP loan - without extensive (and time-consuming) changes to their internal systems. PLUS, as we've seen with the original HARP program, there may be inconsistencies from one servicer to another.

- What will happen to homeowners in the following circumstances:

- Multiple mortgages - second lien holders will have to agree to 're-subordinate' their loan to the newly refinanced loan. While there is no risk to the junior lien holders... we don't know which, if any, second lien holders will agree re-subordinate their mortgages.

- Private Mortgage Insurance Holders - PMI holders have agreed to make the transfer of insurance from one loan to another easier... the details are still being worked out.

Once again... as the guidelines to servicers and lenders will not be available until November 15th... it will take several additional weeks for the lenders and servicers to convert those guidelines into policies and procedures, meaning that it may a couple of months before homeowners can access this new phase of HARP.

Monday, October 3, 2011

Reminder on Deficiency Judgments

The Wall Street Journal published an excellent article this weekend on the dangers of deficiency judgments.

A deficiency judgment is “a judgment lien against a debtor, defendant or borrower whose foreclosure sale did not produce sufficient funds to pay the mortgage in full.”

In plain English: a homeowner can be sued for the difference between the amount the bank received when they auctioned off the house at the Sheriff’s sale, and the amount of the outstanding mortgages.

In the Wall Street Journal article, many of the former homeowners had purchased in Florida, where judgment can be sought on ANY mortgage deficiency. However, Minnesota is a ‘Non-Recourse’ state. This means that FIRST lien holders CANNOT seek judgment (cannot sue) former homeowners for outstanding funds*.

HOWEVER... any “Junior”, or "Second" lien-holders CAN. If there is more than one mortgage on the property – or if there is a line of credit or HELOC taken out against the property – THOSE lenders CAN sue the former property owner for payment of any outstanding debt.

Lenders can take up to SIX YEARS in Minnesota to decide whether or not to sue for any deficiency. In many cases, the lender won't be the ones seeking judgment. They'll simply sell the outstanding deficiency to collections companies, for pennies on the dollar, who will then be relentless in their efforts to collect.

One of the scariest quotes from the article comes from a representative of one of the collection agencies:

"We are waiting for the economy to somewhat heal so that it's a better time to go after people," says Douglas Hannah, managing director of Silverleaf.

The MN Home Ownership Center has a helpful fact sheet on its website about deficiency judgments. You can download the fact sheet here.

Deficiency Judgments are just ONE of the MANY considerations struggling homeowners need to think about when facing a possible foreclosure. If you, or someone you know is struggling with mortgage payments... don't wait until it's too late. To find your local non-profit, FREE Foreclosure Counselor, click here. For additional information about preventing foreclosure in Minnesota, click here.

* There are situations in which a homeowner can open themselves up to deficiency on a first lien. In a short sale situation, if the negotiations aren't carried out properly homeowners may unwittingly sign paperwork that allows the bank to seek judgement. This occurs when the bank is willing to release the lien so a short sale can occur, but does not release the underlying debt. Homeowners that are selling in a short sale situation need to be EXTREMELY careful about the documents they sign before selling.

Thursday, September 29, 2011

Two Minnesota Housing Agencies Receive Expansion Grants

NeighborWorks America invests in expanding services in Minnesota.

On Friday, September 23, NeighborWorks America announced

$3.65 million in grant funding specifically designed for nonprofits to increase

their services for underserved communities by expanding the geographic reach of

programs that have already been successfully established.

NeighborWorks America

hopes this grant funding will help agencies with a track record of successful

programs bring their initiatives to even more communities in need. Among the 25

organizations receiving grant funds are two Minnesota-based agencies: Southwest

Minnesota Housing Partnership and Dayton’s Bluff Neighborhood Housing Services.

The Southwest Minnesota

Housing Partnership works to provide a sufficient supply of adequate, safe, sanitary and affordable

dwellings for the people of southwestern Minnesota and is a member of the

Center’s Homeownership Advisor’s Network.

Dayton’s Bluff Neighborhood Housing Services provides owner-occupied rehab lending and

construction management, homeownership education counseling, financial entry

assistance, purchase-rehab-resale and new construction. Both of these

organizations are making valuable contributions towards enabling successful

homeownership for residents of Minnesota.

Congratulations to both organizations on receiving a

NeighborWorks America grant to continue and expand your good work!

For more

information and a list of all 25 grant recipients, visit the NeighborWorks

America news site.

Wednesday, September 28, 2011

Foreclosure Counseling - NFMC Report

Last week, NeighborWorks America released its 6th report to Congress on the National Foreclosure Mitigation Counseling program (NFMC). The full report is available here.

Once again, the most recent report shows that while foreclosures continue to impact the nation's housing market, foreclosure intervention/prevention counseling WORKS.

Here are just a few of the highlights from the report:

Once again, the most recent report shows that while foreclosures continue to impact the nation's housing market, foreclosure intervention/prevention counseling WORKS.

Here are just a few of the highlights from the report:

- Homeowners who receive foreclosure prevention counseling are 70% more likely to cure their foreclosure than similar homeowners that don't receive counseling.

- Counseling clients that received loan modifications were able to reduce their monthly loan payments an additional $260 MORE than homeowners that don't work with a counselor. The cumulative savings for struggling homeowners? More than $560 Billion (with a "B") dollars PER YEAR.

One of the interesting shifts highlighted in the report is the fact that, for the first time, a majority of the clients nationwide that sought foreclosure counseling (53%) hold fixed-rate mortgages with interest rates below 8%. In October of 2008... only 30% of homeowners were in the same situation. The foreclosure crisis in the U.S. is definitively no longer just a sub-prime issue. Over 60% of homeowners cite unemployment or underemployment as the primary reason they are struggling with their mortgage payment.

All of this information is very similar to the information we've seen in Minnesota. The Center's 2010 report on the foreclosure prevention counseling is available here.

Given that foreclosures in Minnesota have once again begun to tick upwards... it is vitally important that homeowners seek the help of a certified non-profit Housing Counseling agency when they're struggling with their mortgage. Do you know someone that's struggling to make their mortgage payment? Let them know about free counseling in Minnesota by having them visit: www.hocmn.org for more information.

Wednesday, September 14, 2011

Finally - Major Changes in the Mortgage Industry

Major regulatory changes are shaking up the how servicers deal with delinquent homeowners.

The number one complaint the Center hears from struggling homeowners is how difficult it is to work with their bank or servicer. Common complaints include getting lost in overly-complicated voice-mail systems, being routed from one department to another, never being able to speak with the same agent or representative twice, and constantly being told conflicting information when speaking with different agents. However... a major change is on the horizon that should put an end to all this confusion:

The Making Home Affordable (MHA) program has updated their servicer guidance to require a “Single Point of Contact for Borrower Assistance”. In essence, the new guidance requires servicers to provide a single relationship manager to each struggling homeowner that is applying for help through the Making Home Affordable program or any other foreclosure-prevention option. This includes HAMP, HAFA, UP and any in-house modification MHA servicers may provide.

The relationship manager will be responsible for communicating with the borrower, tracking their documents, responding to inquiries and coordinating the communication with any other bank/servicer employees. Homeowners should receive notice about being assigned to a contact as well as a toll-free number to use and information about the preferred method by which they should send documents to the servicer. The guidelines state that the relationship manager must be a full-time employee of the servicer, not a sub-contractor, who should be fully trained on the MHA program and the other in-house loss mitigation options available to clients. Even if the client is not eligible for any loss mitigation options, and the loan is foreclosed, the relationship manager must still be available to the homeowner to answer questions about the status of the foreclosure.

It remains to be seen how well the servicers do implementing these changes, but this is good news for struggling homeowners AND their housing counselors.

Are you, or someone you know struggling with mortgage payments? FREE, non-biased housing counselors are available to help! Don't delay, visit www.hocmn.org to learn more about ways to avoid foreclosure in Minnesota.

The number one complaint the Center hears from struggling homeowners is how difficult it is to work with their bank or servicer. Common complaints include getting lost in overly-complicated voice-mail systems, being routed from one department to another, never being able to speak with the same agent or representative twice, and constantly being told conflicting information when speaking with different agents. However... a major change is on the horizon that should put an end to all this confusion:

The Making Home Affordable (MHA) program has updated their servicer guidance to require a “Single Point of Contact for Borrower Assistance”. In essence, the new guidance requires servicers to provide a single relationship manager to each struggling homeowner that is applying for help through the Making Home Affordable program or any other foreclosure-prevention option. This includes HAMP, HAFA, UP and any in-house modification MHA servicers may provide.

The relationship manager will be responsible for communicating with the borrower, tracking their documents, responding to inquiries and coordinating the communication with any other bank/servicer employees. Homeowners should receive notice about being assigned to a contact as well as a toll-free number to use and information about the preferred method by which they should send documents to the servicer. The guidelines state that the relationship manager must be a full-time employee of the servicer, not a sub-contractor, who should be fully trained on the MHA program and the other in-house loss mitigation options available to clients. Even if the client is not eligible for any loss mitigation options, and the loan is foreclosed, the relationship manager must still be available to the homeowner to answer questions about the status of the foreclosure.

It remains to be seen how well the servicers do implementing these changes, but this is good news for struggling homeowners AND their housing counselors.

Are you, or someone you know struggling with mortgage payments? FREE, non-biased housing counselors are available to help! Don't delay, visit www.hocmn.org to learn more about ways to avoid foreclosure in Minnesota.

Wednesday, August 31, 2011

HUD Extends Application Period for EHLP

EHLP offers an ‘emergency bridge loan’ (mortgage payment assistance) of up to $50,000 for qualified homeowners who have experienced an involuntary reduction in income (due to medical or employment issues) and are at risk of foreclosure.

Several thousand EHLP pre-applications were received during the original enrollment period in July. The majority of those did not meet the strict guidelines established by HUD and the Dodd-Frank Act. Because of the high disqualification rate, HUD anticipates that there will be funding available to reach additional struggling homeowners, and has decided give additional homeowners the opportunity to apply for these funds during an “Open Enrollment” period.

However, homeowners need to understand two key points about this new open enrollment period:

- The strict qualifying guidelines still apply

- Open enrollment requires a COMPLETE application and supporting documentation

The strict guidelines include (but certainly aren’t limited to):

- 90 days late as of June 1, 2011 and homeowners must still be at least 90 days late

- Must have experienced a documentable reduction of 15% in their income due to the economy or a medical condition (involuntary layoff or wage reduction, for example)

- No sheriff’s sale scheduled within the next 30 days

EHLP funds are provided to qualified homeowners on a first-come, first-served basis and it is critical homeowners provide all required application documents as quickly as possible, or they may risk losing the opportunity to apply for assistance. In Minnesota homeowners should submit all documents before 4:00pm on Thursday, September 15th and understand that as the September 15th deadline nears, there may not be enough time to review application documents. Submission of documentation does NOT guarantee that an application will be reviewed or accepted by HUD.

What should interested homeowners do?

Homeowners that are interested in applying for EHLP during the open enrollment period should contact their local Housing Counseling agency that is participating in open enrollment to see if they meet the strict program requirements and for information on how to apply.

- Hennepin County residents, call Community Action Partnership of Suburban Hennepin at (952) 933-1993.

- Carver, Scott & Washington County residents, call Carver County CDA at (952) 658-7878.

- Dakota County Residents, Call Dakota County CDA at (651) 675-4555.

- Residents of ALL OTHER MINNESOTA Counties, call LSS Financial Counseling at (800) 777-7419.

Additional information about EHLP and the strict eligibility requirements are also available on the EHLP Minnesota website: www.EHLPMinnesota.com.

Wednesday, August 3, 2011

Homeownership Issues & The 2011 Legislative Session

This post is a guest post by Laura Hodges, AmeriCorps Member with the MN Home Ownership Center:

|

| Click To Enlarge (c) inspidlife (Used Under Creative Commons License) http://www.flickr.com/photos/soaptrail/ |

2011 Legislative Update

The 2011 legislative session at times got hotter than a July weekend. Combining that with the government shut down, Minnesota citizens might have questioned if the politicians were getting anything done.

Well I am happy to report that lawmakers implemented two agreements during the most recent legislative session that offer additional protections to homeowners beginning August 1, 2011:

Mortgage Ownership Disclosure (Link)

This law updates an existing law that requires mortgage servicers to disclose to a borrower, upon request, who actually owns their mortgage loan and the contact information. While this may be helpful for homeowners, it is especially helpful for Homeownership Advisors (foreclosure counselors) when working with homeowners facing foreclosure as the knowledge of who really owns the loan can be helpful when negotiating workout options.

Extended Redemption Period for Reverse Mortgage Holders

The other change that was passed during the legislative session involves Reverse Mortgages. The law grants reverse mortgage borrowers, who have had a sheriff sale due to foreclosure, an extended redemption period of 12 months. This extension will give time for the homeowner to regain ownership if they can pay off the mortgage loan in full, or can be used as extended time to find alternative housing options. This change is welcome news for many reverse mortgage holders.

The Minnesota Homeownership Center would like to thank Laura for her valuable contributions to our work and mission over the past year. You've been a great member of our team, and we wish you the best as you move on to pursue other goals!

Tuesday, July 19, 2011

Court Ruling in Rochester May Affect Foreclosures in Minnesota

When you think of Rochester Minnesota - you may think of the winding Zumbro river, the large IBM site or, of course, the Mayo Clinic. It's not often you think of Rochester as a setting for courtroom drama that may change the way banks and their attorneys handle foreclosures. However, a recent court decision in Olmsted County may do just that.

A foreclosure that had taken place in August of 2010 was ruled invalid by Olmsted County District Judge Jodi Williamson, because the Notice of Foreclosure Sale (Sheriff's Sale) was posted in a small newspaper in a neighboring township - not in a publication distributed in the area where the house was located.

The State of Minnesota requires that lenders notify homeowners of a pending sale by attempting to serve the occupant of the property with the Sale Notice (via local Sheriff or process server) AND publish, for 6 consecutive weeks, the date and location of the sale in a local publication.

According to housing counselors in the Rochester area, many attorneys use the smaller nearby papers due to the costs of publishing foreclosure notices in the Rochester paper. According to sources, the cost to publish a foreclosure notice in the Rochester Post Bulletin was the highest in the state.

If this ruling holds, it will mean that some foreclosures that took place in Rochester will be ruled invalid.

However, this won't be the end of foreclosures in Rochester as:

It's still great to see that Minnesota is "ahead of the curve" when it comes to consumer protections under the law. Even when a bank must proceed with a foreclosure - if there are no other options - they must comply with the law.

If you're a homeowner struggling with your mortgage - don't wait for a legal ruling or hope for a legal loophole to avoid facing your foreclosure issue - non-profit (free) housing counseling is available throughout the state - including Olmsted County - to help YOU avoid foreclosure. Don't delay, visit the Minnesota Home Ownership Center's website HERE to find your local counselor.

A foreclosure that had taken place in August of 2010 was ruled invalid by Olmsted County District Judge Jodi Williamson, because the Notice of Foreclosure Sale (Sheriff's Sale) was posted in a small newspaper in a neighboring township - not in a publication distributed in the area where the house was located.

The State of Minnesota requires that lenders notify homeowners of a pending sale by attempting to serve the occupant of the property with the Sale Notice (via local Sheriff or process server) AND publish, for 6 consecutive weeks, the date and location of the sale in a local publication.

According to housing counselors in the Rochester area, many attorneys use the smaller nearby papers due to the costs of publishing foreclosure notices in the Rochester paper. According to sources, the cost to publish a foreclosure notice in the Rochester Post Bulletin was the highest in the state.

If this ruling holds, it will mean that some foreclosures that took place in Rochester will be ruled invalid.

However, this won't be the end of foreclosures in Rochester as:

- Many homeowners would have been notified via process server anyway, and

- Most lenders will simply refile the foreclosure, obtain a new sale date from the Sheriffs Department and notify homeowners again, this time complying with the state statute.

It's still great to see that Minnesota is "ahead of the curve" when it comes to consumer protections under the law. Even when a bank must proceed with a foreclosure - if there are no other options - they must comply with the law.

If you're a homeowner struggling with your mortgage - don't wait for a legal ruling or hope for a legal loophole to avoid facing your foreclosure issue - non-profit (free) housing counseling is available throughout the state - including Olmsted County - to help YOU avoid foreclosure. Don't delay, visit the Minnesota Home Ownership Center's website HERE to find your local counselor.

Thursday, July 7, 2011

New Video - Emergency Homeowners' Loan Program

The Minnesota Homeownership Center has created a new video to assist consumers in understanding the new Emergency Homeowners' Loan Program.

As yesterday's post mentioned, under EHLP 1,405 selected (unemployed/underemployed) Minnesota homeowners will receive up to $50,000 in interest-free loans over the next two years to help pay mortgage costs. The loans are also 100% forgivable for homeowners who stay in their home for 5 years following the program’s completion.

The program can be a little difficult to understand, as it has very strict qualification guidelines and actually rolls out in several phases over the next few months. MN Housing and the MN Homeownership Center have created a website: www.EHLPMinnesota.com to try and outline some of the program guidelines and explain to consumers how the program works.

NOW, the Center has added a new video that explains, in seven short minutes, the basics of the EHLP program and how to apply.

Please feel free to share this video or embed it on your website! If you do share it, please let us know in the comments or by email: ed@hocmn.org.

Here's the video:

To link to the video from your site, blog or email, use: http://youtu.be/qtQ2NBlxYFE

To embed the video on your site, visit the link above and click on the "Share" button below the video.

As yesterday's post mentioned, under EHLP 1,405 selected (unemployed/underemployed) Minnesota homeowners will receive up to $50,000 in interest-free loans over the next two years to help pay mortgage costs. The loans are also 100% forgivable for homeowners who stay in their home for 5 years following the program’s completion.

The program can be a little difficult to understand, as it has very strict qualification guidelines and actually rolls out in several phases over the next few months. MN Housing and the MN Homeownership Center have created a website: www.EHLPMinnesota.com to try and outline some of the program guidelines and explain to consumers how the program works.

NOW, the Center has added a new video that explains, in seven short minutes, the basics of the EHLP program and how to apply.

Please feel free to share this video or embed it on your website! If you do share it, please let us know in the comments or by email: ed@hocmn.org.

Here's the video:

To link to the video from your site, blog or email, use: http://youtu.be/qtQ2NBlxYFE

To embed the video on your site, visit the link above and click on the "Share" button below the video.

Wednesday, July 6, 2011

New Foreclosure Prevention Assistance Program - EHLP

The program is only accepting applications between July 5 & July 22. Under this program, more than 1,400 selected Minnesota homeowners will receive up to $50,000 in interest-free loans over the next two years to help pay mortgage costs. The loans are also 100% forgivable for homeowners who stay in their home for 5 years following the program's completion.

Homeowners eligible to apply for the federal program must meet several criteria, including:

- Have faced an income decline of at least 15% due to involuntary unemployment, underemployment or medical issues

- Have been unable to make their mortgage payment for at least 3 months prior to June 1, 2011

- Reside in the mortgaged property

Unemployed or underemployed homeowners should visit the program's Minnesota website at www.EHLPMinnesota.com to learn more about the program, verify eligibility and download a pre-application.

Remember: The deadline to apply for this one-of-a-kind program is 4:30p.m. on Friday, July 22.

Homeowners are also being warned to steer clear of scams. There is no charge to apply for EHLP and checking eligibility and filling out the pre-application is simple. An offer to help fill out EHLP forms for a fee or anyone who guarantees that a pre-application will result in acceptance in the program in exchange for money is a scam.

Visit www.EHLPMinnesota.com for more information.

------------------------------------------------------------------------------------------------------

CALL TO ACTION: Help Us Spread The Word!

If you know of unemployed/underemployed homeowners who are struggling with mortgage payments, we ask that you spread the word to them about this unique, and short-lived, opportunity.

Below you will find additional tools that you can use to help spread the word (Links to documents):

- Fact Sheet for Professionals - Understanding EHLP (PDF)

- A handout for consumers (PDF)

- Email text that you can customize to your constituents/clients (MS Word)

- Electronic newsletter or blog post text. (MS Word)

Maybe a link on your website? An email to friends/family or clients? A handout at the cash register or inserted into clients purchases? A blog post on your company or personal blog? WHATEVER! We'd love to hear about it! Post a comment about how you're helping, or visit our Facebook page and share your outreach ideas. THANKS!

Tuesday, May 24, 2011

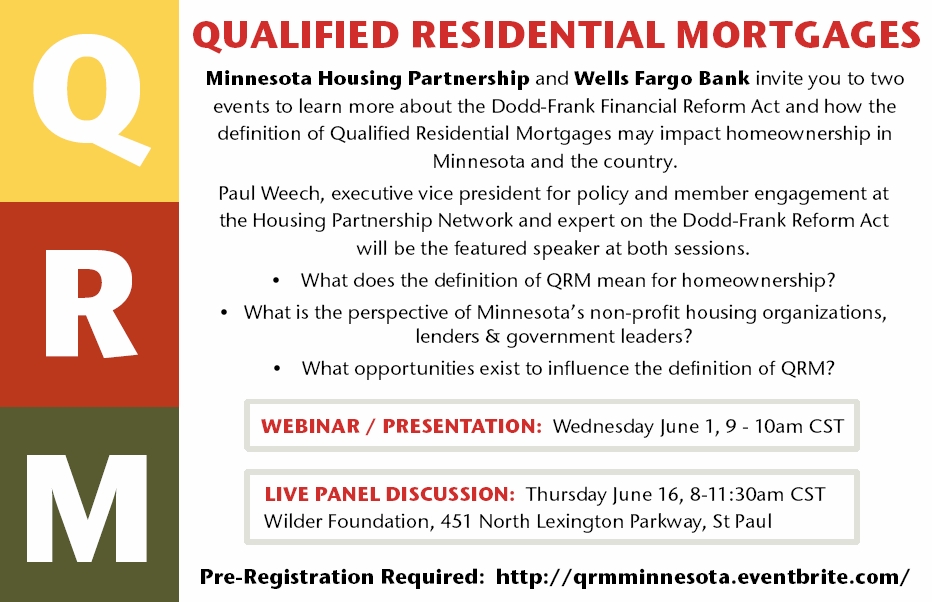

Dodd-Frank Reform Act & QRM Impact on Minnesota

Training for Housing, Lending & Real Estate professionals.

On Tuesday, May 24th, the Minneapolis/St. Paul Business Journal reported that, according the Federal Reserve Bank of Minneapolis, one in three banks in Minnesota are still struggling to recover from the foreclosure/financial crisis.

On Tuesday, May 24th, the Minneapolis/St. Paul Business Journal reported that, according the Federal Reserve Bank of Minneapolis, one in three banks in Minnesota are still struggling to recover from the foreclosure/financial crisis.

With this backdrop... Minnesota's mortgage lenders now face the uncertainties created by the implementation of the definition of "Qualified Residential Mortgage" (Section 941) of the Dodd-Frank Reform Act. This section of the Act will require all financial institutions that securitize mortgage loans to retain at least five percent of the credit risk, and proposes strict definitions for Qualified Residential Mortgages that can be securitized.

Two of the Minnesota Homeownership Center's partners, Minnesota Housing Partnership and Wells Fargo will be hosting two events offering affordable housing advocates, lending and Real Estate professionals the opportunity to learn more about the Dodd-Frank Financial Reform Act and how the definition of Qualified Residential Mortgages may impact affordable homeownership in Minnesota and the country.

Paul Weech, executive vice president for policy and member engagement at the Housing Partnership Network and expert on the Dodd-Frank Reform Act will be the featured speaker at both sessions.

Participants will learn about:

SESSION 1: Webinar

Date & Time: Wednesday, June 1st, 9-10am CST

SESSION 2: Live Panel Discussion

Date & Time: Thursday, June 16th, 8 - 11:30am CST

Location: Wilder Foundation, St. Paul, MN

To register (pre-registration required) or to learn more about the topics covered, visit the registration page here: http://qrmminnesota.eventbrite.com/

With this backdrop... Minnesota's mortgage lenders now face the uncertainties created by the implementation of the definition of "Qualified Residential Mortgage" (Section 941) of the Dodd-Frank Reform Act. This section of the Act will require all financial institutions that securitize mortgage loans to retain at least five percent of the credit risk, and proposes strict definitions for Qualified Residential Mortgages that can be securitized.

Two of the Minnesota Homeownership Center's partners, Minnesota Housing Partnership and Wells Fargo will be hosting two events offering affordable housing advocates, lending and Real Estate professionals the opportunity to learn more about the Dodd-Frank Financial Reform Act and how the definition of Qualified Residential Mortgages may impact affordable homeownership in Minnesota and the country.

Paul Weech, executive vice president for policy and member engagement at the Housing Partnership Network and expert on the Dodd-Frank Reform Act will be the featured speaker at both sessions.

Participants will learn about:

- What does the definition of QRM mean for homeownership?

- What is the perspective of Minnesota’s non-profit housing organizations, lenders & government leaders of QRM?

- What opportunities exist to influence the final definition of QRM?

SESSION 1: Webinar

Date & Time: Wednesday, June 1st, 9-10am CST

SESSION 2: Live Panel Discussion

Date & Time: Thursday, June 16th, 8 - 11:30am CST

Location: Wilder Foundation, St. Paul, MN

To register (pre-registration required) or to learn more about the topics covered, visit the registration page here: http://qrmminnesota.eventbrite.com/

Friday, May 20, 2011

New Mortgage Disclosure Forms

Share your opinion with the Consumer Financial Protection Bureau

It’s not very often that the general public gets to weigh in on items that will affect the entire mortgage industry. Recently, the Consumer Financial Protection Bureau (CFPB) released drafts of a new one-page (two-sided) mortgage disclosure form and is asking for YOUR opinion. The final form will combine the two mortgage disclosures that are currently required -- the federal Truth in Lending Act (TILA) mortgage disclosure and the Real Estate Settlement Procedures Act (RESPA) Good Faith Estimate -- into one two-page form, down from the current five pages.

It’s not very often that the general public gets to weigh in on items that will affect the entire mortgage industry. Recently, the Consumer Financial Protection Bureau (CFPB) released drafts of a new one-page (two-sided) mortgage disclosure form and is asking for YOUR opinion. The final form will combine the two mortgage disclosures that are currently required -- the federal Truth in Lending Act (TILA) mortgage disclosure and the Real Estate Settlement Procedures Act (RESPA) Good Faith Estimate -- into one two-page form, down from the current five pages.

While these forms are covered in-depth in the Home Stretch workshop, they certainly can be confusing for the average homebuyer, and the CFPB is asking the general public to offer their opinion on which of the two is easier for you (or your customers) to understand.

Both versions show the key loan terms like the interest rate, the monthly loan payment, any closing costs and taxes. Borrowers can quickly see how much they'll be paying per month, and, if the loan is adjustable, how those payments might change throughout the life of the loan.

Interestingly, the form also shows the Annual Percentage Rate (APR) paid over a five-year period, along with the amount of principal you will have paid off in five years (real equity).

The CFPB will be working on these forms until July of 2012, but over the next few months, the agency will be revising and re-uploading the form(s) on its site based on the input it receives.

So… go vote! Let your opinion be heard. Then come back and let us know which one you prefer in the comments. The two forms are available here.

When comparing the forms, we recommend that you focus on what information mortgage lenders and/or brokers should share with homebuyers to make the process as easily understood and transparent as possible. Remember… our goal at the Minnesota Home Ownership Center, and of our lender and real estate partners, is successful homeownership. Which form do you think will best help potential buyers in that respect?

Are you a Minnesota resident thinking of buying your first home? Do terms like TILA, RESPA and GFE sound like a foreign language? You can learn more about these, and many more, terms, the mortgage loan process and the best steps to follow to be a successful homeowner by taking a Home Stretch workshop. For more information, click here.

While these forms are covered in-depth in the Home Stretch workshop, they certainly can be confusing for the average homebuyer, and the CFPB is asking the general public to offer their opinion on which of the two is easier for you (or your customers) to understand.

Both versions show the key loan terms like the interest rate, the monthly loan payment, any closing costs and taxes. Borrowers can quickly see how much they'll be paying per month, and, if the loan is adjustable, how those payments might change throughout the life of the loan.

Interestingly, the form also shows the Annual Percentage Rate (APR) paid over a five-year period, along with the amount of principal you will have paid off in five years (real equity).

The CFPB will be working on these forms until July of 2012, but over the next few months, the agency will be revising and re-uploading the form(s) on its site based on the input it receives.

So… go vote! Let your opinion be heard. Then come back and let us know which one you prefer in the comments. The two forms are available here.

When comparing the forms, we recommend that you focus on what information mortgage lenders and/or brokers should share with homebuyers to make the process as easily understood and transparent as possible. Remember… our goal at the Minnesota Home Ownership Center, and of our lender and real estate partners, is successful homeownership. Which form do you think will best help potential buyers in that respect?

Are you a Minnesota resident thinking of buying your first home? Do terms like TILA, RESPA and GFE sound like a foreign language? You can learn more about these, and many more, terms, the mortgage loan process and the best steps to follow to be a successful homeowner by taking a Home Stretch workshop. For more information, click here.

Subscribe to:

Posts (Atom)