An anonymous commenter posted a question on our February 4th blog post regarding deficiency judgments (Sued – After a Foreclosure). It’s not often we receive a question that we can’t answer quickly… so we thought we’d post the commenter’s question, and the answer, here:

I have a weird one for you. What happens if the Sheriff sale nets more than you owe? Our house was auctioned on Tuesday. We owe $360,000 and it sold for $403,000.

Given the current housing environment in Minnesota… this situation doesn’t happen very often… so we had to run the question by one of the Center’s partners, the Housing Preservation Project. Attorney Jane Bowman of the Foreclosure Relief Law project helped us with the following information. (Thanks, Jane!)

The vast majority of residential mortgages in Minnesota are foreclosed through a process known as Foreclosure by Advertisement (for more information on this process, the Center has a fact-sheet/process chart, here).

In a foreclosure by advertisement, if there is a surplus after a sheriff’s sale, the borrower receives the surplus. However, as often is the case, the devil is in the details. In this case, the important detail is how the word “surplus” is defined.

Before a surplus is established, there is a list of entities that take their cut BEFORE the homeowner:

- The cost of the foreclosure sale is covered,

- All late payments are paid (with interest),

- Any outstanding taxes and insurance are paid,

- The remaining amount of the first mortgage is satisfied,

- Then any junior lienors get paid (HELOCs, lines of credit, second mortgages, etc.)

If at this point there is a surplus, then the borrower gets the surplus.

For those of you that would like to dig into the statutes, the relevant statutes are available on-line here: 580.09, 580.10 (581.06 covers surplus amounts in a judicial foreclosure).

The statute is silent as to how the borrower would actually get paid… and how to request an surplus funds. After discussing this with Jane and other specialists, we’ve concluded that the local Sheriff’s office more than likely oversees the payment distribution, and if you believe you have a surplus due, you should contact the Sheriff’s office on how to proceed.

There is also another ‘wrinkle’ in this situation… as there may be tax implications of any surplus as well! As it doesn’t happen often… we are unclear on how Uncle Sam would treat the gross surplus amount (in our commenter’s case, would the full $43,000, not the surplus amount after all payments have been made, be considered income?). Any tax specialists like to share their knowledge with us in the comments?

All-in-all… it is most likely that our commenter will see very little, if any, of the ‘surplus’ amount from the Sheriff’s sale, but still may have tax issues on those funds.

As we've mentioned before... one of the most important steps to becoming a successful homeowner is efficient and effective money management. In fact, understanding finances and credit is a large segment of what is taught in the Home Stretch workshop.

Part of successful money management is the ability to save and prepare for FUTURE homeownership-related expenses. The general 'rule-of-thumb' is to save between 1-2% of your home's purchase price EVERY year for future maintenance and upkeep on the home. (Eventually, even brand new homes will need repairs and replacement of major systems like the furnace, A/C, roof, etc.).

Fixr.com has put together an AMAZING infographic showing how Americans typically spend their money on home improvement based on data from The American Housing Survey, the US Census, The National Bureau of Economic Research, and the Joint Center for Housing studies at Harvard.

According to their data, Americans spent $42 billion dollars on home improvements in 2009 - and that's down from the $49 billion they spent in 2008.

Here's their graphic:

(Click image to enlarge - it's HUGE)

(Click image to enlarge - it's HUGE) Click image to enlarge

Click image to enlarge

Source: Here

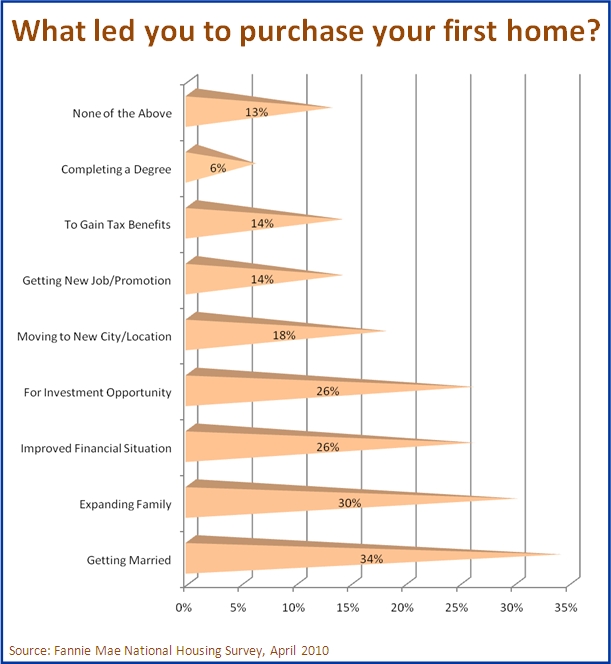

One of the first steps in a Home Stretch workshop is to explain to potential home buyers the advantages and disadvantages of homeownership. The workshop actually starts by having people think through some of the reasons WHY they'd like to be homeowners.

Fannie Mae's 2010 National Housing Survey asked that same question of thousands of people across the country... "What led you to purchase your first home?" (Translation: Why'd you become a homeowner?). The results are shown here:

(Click Image to Embiggen)

(Click Image to Embiggen) (Click Image to Embiggen)

(Click Image to Embiggen)

Fannie Mae has released its 2010 "National Housing Survey"!

The Survey, conducted in December 2009 and January 2010 (so the data is fairly recent)... surveyed consumer perspectives on a range of related issues, including: current attitudes toward the economy and housing; present conditions for homeownership; owning versus renting; the present climate for borrowing; current mortgage satisfaction; the impact of being "underwater" on borrowers; and attitudes toward defaulting. In some instances, data are compared to a 2003 study on housing by Fannie Mae.

Over the next few weeks... we'll be highlighting some of the findings of the survey.

Here's the first highlight: Reasons for Buying a Home:

Nearly two-thirds (65 percent) of survey respondents prefer owning to renting, citing non-financial reasons such as safety (43 percent) and quality of local schools (33 percent) as driving factors in wanting to own a home.

Here's the breakdown of responses:

(Click Image to Enlarge)

(Click Image to Enlarge)

We all know that house prices have dropped in Minnesota over the past year or so, and in some areas those drops have been dramatic. While painful for people who purchased at the height of the market, there is a silver lining: as home prices have dropped, the ‘qualifying income’ needed to purchase a median-priced home in Minnesota has dropped as well.

Simply put: homes are more affordable now for (prepared!) buyers than in recent memory.

According to the “Paycheck to Paycheck: Housing Affordability Report” from the Center for Housing Policy (CHP), buyers of median-priced homes in two metro areas in Minnesota needed less income in 2009 than in 2008.

“Qualifying Income”, according to CHP is “the income required to qualify for a mortgage on the median priced home by assuming a 90 percent loan-to-value ratio — that is, a 10 percent down-payment plus the use of private mortgage insurance. Monthly payments are calculated to include loan principal and interest as well as estimated taxes and insurance. These payments are annualized and assumed to comprise no more than 28 percent of annual income in accordance with conventional underwriting guidelines.”

That means that in 2008, in order to purchase a median-priced home in the Twin Cities of Minneapolis and St. Paul, homebuyer(s) needed a minimum income of just over $59,000.00. In order to afford a median-priced home in 2009, however, the qualifying income had reduced over 14% to just over $50,000.

Here’s a chart from the data for both Mpls/St. Paul and the Duluth Metro areas:

(Click Image To Enlarge)

In addition... there are more programs than ever to assist with down-payment and other entry costs. Does this mean everyone should run out a purchase home now while they’re more affordable? NO, of course not.

Affordability is only one of the MANY considerations homebuyers need to be thinking about when purchasing a home. Others include:

- Long term commitment

- Willingness to undertake maintenance & repairs

- Possible depreciation (2005 – 2009, for example)

- Time required to sell

...And many others.

Before jumping in to homeownership... even with prices as affordable as they are, potential homebuyers need to fully understand the advantages and disadvantages of homeownership. Are you thinking about buying a home in Minnesota? Your first step is to speak with a non-profit Housing Counselor or learn more about the home ownership process in Minnesota by taking a Home Stretch workshop.

Arm yourself with information before proceeding with one of the largest purchases you may ever make!

According to the research firm Fiserv, Inc. ... Twin Cities Metro Area home prices won't recover to their mid-2000's peak until sometime between 2015 and 2025. Yeah... that's 15 years from now!

Minneapolis was actually highlighted in their press release (but not in the data they've released for free, sorry):

A protracted recovery in home prices is also expected in many urban neighborhoods where predatory lending was most rampant. There, home prices rose rapidly from very low levels during the bubble years. These markets include neighborhoods in cities such as Minneapolis, Memphis and Chicago. [Emphasis ours]

Here's the 'heat map' for housing-price recoveries according to Fiserv:

(Click To Enlarge)

(Click To Enlarge)- The idea of earning quick equity and/or using your home as short-term road to wealth should NEVER be a deciding factor in purchasing your first home;

- Purchasing a home is a LONG-TERM decision... you may not be able to sell the home you purchase today FOR YEARS without incurring expenses;

- Home ownership is expensive and homeowners need to understand the costs as well as the benefits of owning;

- Pre-purchase education and counseling are keys to understanding REAL wealth generation and long-term successful homeownership. Click here for more info on the Home Stretch program.

For current homeowners (and the foreclosure issue):

- Without price appreciation on the horizon for a number of years, struggling homeowners will be unable to access equity, or sell without incurring losses, for quite some time.

- More homeowners may decide to 'strategically default' that may lower prices even further, which in turn will further depress home prices in hard-hit areas.

ALSO... we couldn't post about foreclosure issues without warning Minnesota Home Owners, AGAIN, to make sure that they NEVER pay for any third-party loan modification service. Deal directly with your lender yourself, or with one of our free, non-profit Foreclosure Counselors.

Any thoughts? Feel fee to share your opinions in the comments.

There’s new research out on the foreclosure rates on low-income buyers that have participated in an IDA (Individual Development Account). The research study, involving over 800 IDA homebuyers, found that nearly all of these buyers were still in their homes and that they had fared far better than similar homebuyers in terms of foreclosure rates and mortgage terms.

The full report, funded by NeighborWorks America and the Ford Foundation, can be viewed here.

Individual Development Accounts are special savings accounts that can be used only for specific qualifying purchases such as a first home, starting a business, or for educational or job training expenses.

Accounts are held at local financial institutions and contributions/deposits made by lower income participants are matched, in some cases 3-to-1, using both private and public sources.

So what makes an IDA homebuyer different from other low-income buyers? Your input is welcome in the comments… but here are some ideas:

- IDA buyers must take financial literacy classes as a requirement of their participation

- IDA buyers must take an approved homebuyer education workshop (like HomeStretch) before purchasing their home

- IDA buyers, through their participation in the program, have learned to work with support network (volunteers, non-profit staff, bankers, etc.) and so they know where to turn for help when facing a financial struggle

Any other ideas? And what does this study mean for other low-income buyers? We welcome your comments!

If you aren't familiar with the MN Home Ownership Center's website... we have a form/widget installed on several pages of the site that allows people to send us questions about their housing situation. A few days ago the Center received a comment through our online form that I thought I'd share with all of you:

Hi, I wish I knew about your organization before I was put in a position where I was given poor advice by my real estate agent on my short sale of my home. I was told by [my agent] to sign a lien release at closing and that would be the same as a satisfaction of debt agreement but afterward my old mortgage comapny informed me that I owe the deficiency balance and now I have to file bankruptcy. do you know of anyway out of this situation so I dont have to file bankruptcy ? I can't afford to pay back the 145,000.00 dollars they want me to pay. Thanks for your time-

We've been able to connect this consumer with a Housing Counselor that may be able to refer the client on for free legal services... but the sad fact is that there is probably nothing that can be done for this client now... short of declaring bankruptcy.

$145,000 is an expensive mistake to make... and we hope that this homeowner's sad tale will help motivate other homeowners that are struggling with their mortgage to seek the FREE, non-biased advise and support of a non-profit Housing Counselor. For more information about the statewide network of Housing Counselors in Minnesota, click here.

Did you know that April is officially "National Financial Literacy Month"?

It's not often we get to quote the President of the United States on our home ownership blog, but in his press release on the announcement about Financial Literacy Month, the President had this to say:

While our Government has a critical role to play in protecting consumers and promoting financial literacy, we are each responsible for understanding basic concepts: how to balance a checkbook, save for a child's education, steer clear of deceptive financial products and practices, plan for retirement, and avoid accumulating excessive debts. [Emphasis Added]

and

I call upon all Americans to observe this month with programs and activities to improve their understanding of financial principles and practices.

Looking for 'programs and activities' to help you understand the financial concepts necessary for successful homeownership? Perhaps you are struggling with your mortgage payment or trying to balance all your financial obligations? The MN Home Ownership Center's website is a great resource! Visit our site today.